Beta distribution¶

It can be viewed as a generalization of a Uniform distribution over the interval \([0,1]\) where the pdf is non constant.

Describes the probability of success in a binomial trial, and it is defined in the range \(<0,1>\). This makes it ideal for modeling proportions and percentages.

We recover the uniform distribution on [0,1] by: $\( Unif(0,1) = Beta(1,1) \)$

PDF¶

\(0 \le \theta \le 1\)

\(\alpha\) - is the shape parameter and it measures the number of successes in an binomial trial \(\alpha -1\)

\(\beta\) - is the shape parameter and it measures the number of failures in an binomial trial \(\beta -1\)

\(B(\alpha,\beta)\) is the beta function and it is an normalization constant

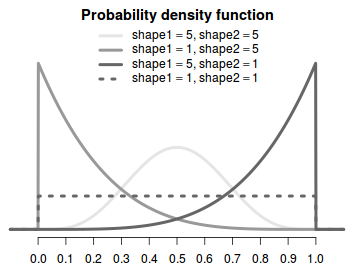

If \(a < 1\) and \(b < 1\)then the PDF is U shaped and opens upward

If \(a > 1\) and \(b > 1\) then the PDF is U shaped and opens down.

If \(a = b\), then the PDF is symmetric about \(1/2\)

If \(a > b\) then the PDF favors values larger than \(1/2\)

If \(a < b\) then the PDF favors smaller than \(1/2\)

Constructing an beta from its mean and sd¶

Moments¶

Mean¶

Variance¶

Mode¶

Properties¶

\(\alpha = \beta\) the distribution is symmetric about \(\theta\)

\(\alpha = \beta = 1\) the distribution is uniform \(\alpha = 0, \beta =1\)

Variance is inversely proportional to the total \(\alpha + \beta\) (the total number of trials)