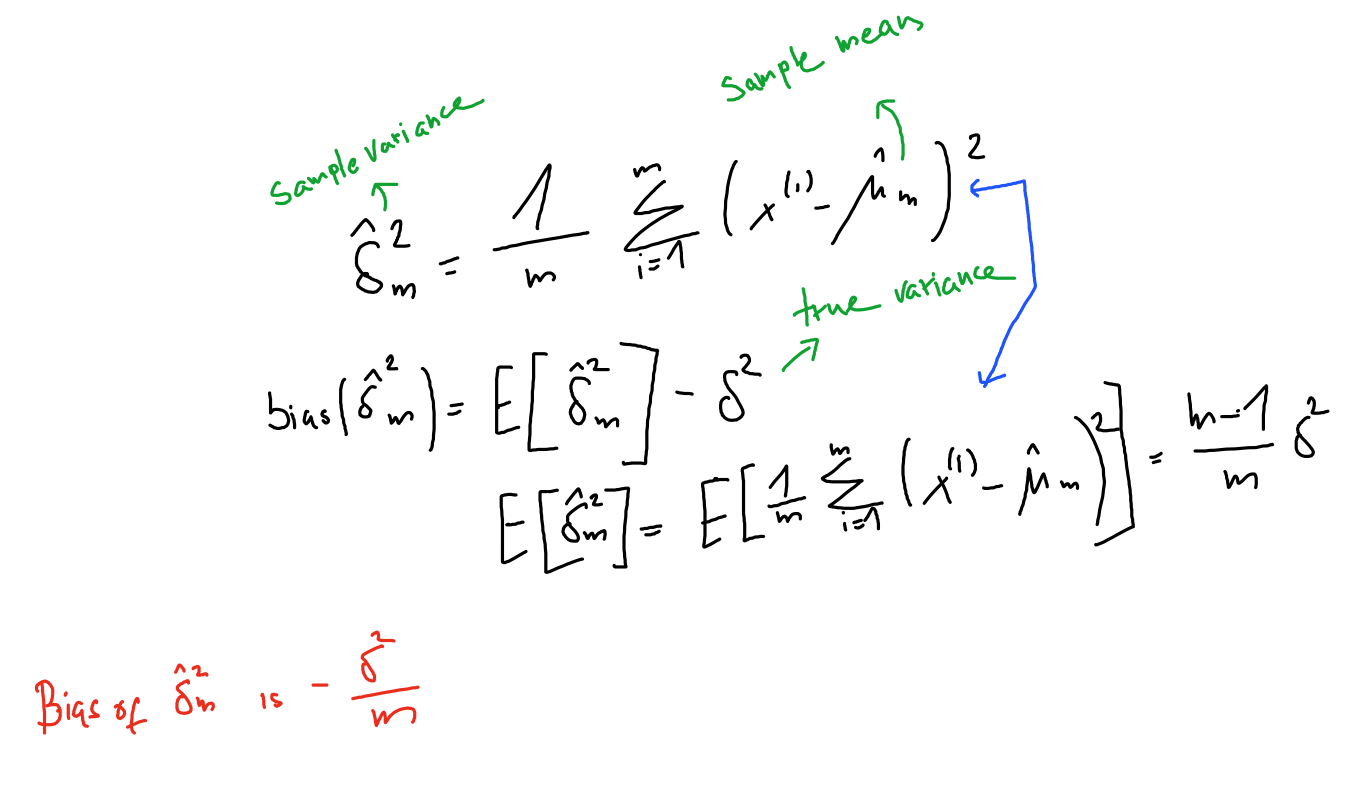

Sample variance¶

We define the sample variance as: $\( \hat{\sigma}^2_m = \frac{1}{m} \sum_{i=1}^m (x^{(i)} - \hat{\mu}_m)^2 \)$

Bias¶

The sample variance is a biased estimator

\[

\text{bias}(\hat{\delta}^2_m) = - \delta^2/m

\]

\(m\) is the number of samples

\(\delta^2\) is the true variance

If we want an unbiased estimator for variance we have:

\[

\tilde{\delta}^2 = \frac{1}{m-1} \sum_{i=1}^m (x^{(i)} - \hat{\mu}_m)^2

\]